TRID – New Lender Disclosure: A benefit to consumers?

Changes are coming with how lenders will be required to disclose information to you prior to closing on the purchase of a home after October 3rd. The original date for this to be enacted was August 1st, but now they bumped it to October and don’t be surprised if it gets pushed again. No worries though, as from what I’ve seen so far this will help consolidate and clarify to consumers just exactly what you are getting involved with when taking out a mortgage.

The harder part comes with the realtors and lenders who will have to digest this and plan accordingly when writing offers as this will likely add some time to the contract period before closing. I thought I would give a quick rundown of what’s involved and how it might impact any future real estate dealings you might have.

What is TRID?

This dates back to the Dodd Frank Act, where they directed the Consumer Financial Protection Bureau (CFPB) to implement regulations to combine the Truth in Lending Act (TILA) and Real Estate Settlement Procedures Act (RESPA) in order to simply this for consumers taking out a mortgage. The four disclosures to review for the real estate transaction process have now been consolidated into two disclosures; the Loan Estimate (LE) and Closing Disclosure (CD).

How does this impact me?

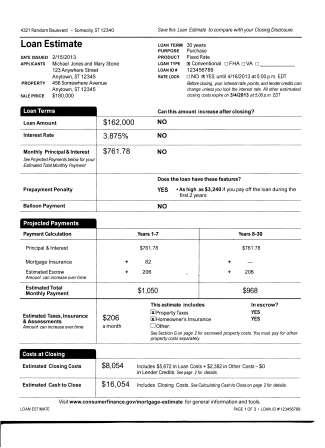

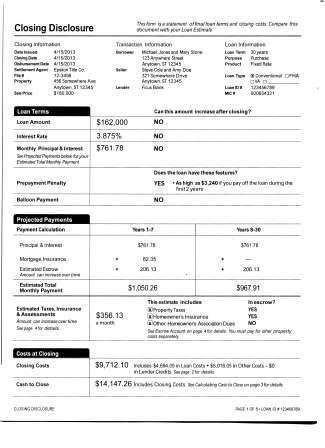

As you will see at the end of this article, I attached a sample page from each new disclosure to help give you a feel for how this might impact you. Personally, I think it will help the consumer out more by really spelling things out in a easy to read format.

The other good thing this does is it brings with it a disclosure period, where the consumer will need the Closing Disclosure (CD) three prior to closing. Now, this is where it might get a little sticky and why you’ll want to be working with a real estate AND lending professional who is up to speed on this stuff. The lender is considered to have delivered this to you after the third day they mailed it to you. Confused? Essentially, the lender mails this to you in regular mail on a Monday. You will have assumed to have received within three business days (Saturdays are included), it will be assumed you received by that Thursday. You then have another three days to review before closing which would take you to the following Monday for the earliest closing date.

Long and short of this is you could be adding an additional week to the contract period to make sure the lender is satisfying these new requirements. I think this will also help closings proceed more smoothly as lenders and title companies cannot be waiting until the last minute to push things through, as some of us have likely experienced before.

Try not to worry if this didn’t all sink in that much, as a good professional will help you through this on top of the deluge of stuff you already need to get through in a real estate transaction.

What if I’m paying cash for a property?

The good news if you aren’t involved in using a mortgage, none of this applies and you can proceed with a quick closing as usual. There are also a few types of mortgages this may not apply to. The best thing to do is consult with your lender and real estate professional and they can help guide you through this.

Remember if you ever need any help with your real estate needs; please consider using us a resource!

Sample of new disclosures: